Dublin, April 07, 2026 (GLOBE NEWSWIRE) -- The "Middle East Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026-2031)" has been added to ResearchAndMarkets.com's offering.

The Middle East Construction Chemicals Market is set to reach USD 6.39 billion in 2026, growing from USD 6.09 billion in 2025. By 2031, projections forecast an increase to USD 8.14 billion, reflecting a CAGR of 4.96% over the 2026-2031

This growth is driven by sovereign wealth fund investments, aligned with national Vision programs, moving away from oil dependency, and technical regulations favoring high-performance, low-emission formulations.

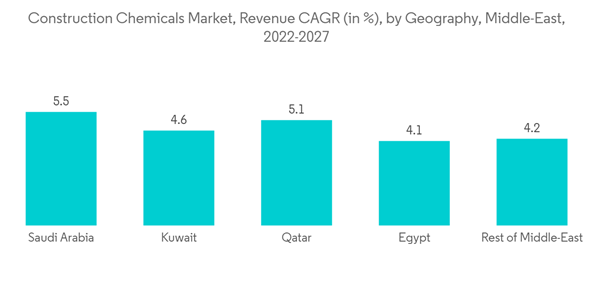

Projects in Saudi Arabia, the UAE, and Qatar form a robust demand backbone for concrete admixtures, waterproofing systems, and corrosion-resistant coatings. Suppliers with long-term framework agreements, multi-phase performance guarantees, and low-VOC documentation capture premium pricing, as consolidation reinforces scale advantages. Competitive barriers rise as developers demand full-cycle supply security, local content, and compliance with green-building mandates.

Middle East Construction Chemicals Market Trends and Insights Accelerated Infrastructure Spending under National Vision Programs

Vision strategies drive unprecedented public-sector funding, establishing multi-year pipelines for infrastructure projects. Saudi Arabia alone invests over USD 1.1 trillion in initiatives like NEOM and Red Sea Global, significantly boosting construction-chemicals consumption baselines. Developers negotiate long-term supply commitments to mitigate phase-overlap risks, spiking bulk admixture demand. The UAE's Al Maktoum International Airport expansion sharpens inter-GCC competition, firming unit prices and stabilizing regional order books.

Mandated Adoption of Green Building Rating Systems

Regulations such as Abu Dhabi's Estidama Pearl and Qatar's GSAS embed eco-compliance into project approvals. The UAE climate law mandates greenhouse-gas disclosures, pushing contractors to seek environmental product declarations. Multinationals lead with water-borne technologies, maintaining performance while reducing solvent levels, securing preferred-supplier status and specification lock-ins.

Tightening VOC-Emission Caps on Solvent-Borne Products

Regional adoption of U.S. EPA aerosol-coating standards forces reformulation or withdrawal of high-VOC materials. Smaller suppliers retreat to low-margin commodity lines, while large players leverage aqueous systems to retain mechanical performance. Contractors tangle with application adjustments, but non-compliance penalties outweigh adaptation costs.

Market Drivers and Restraints

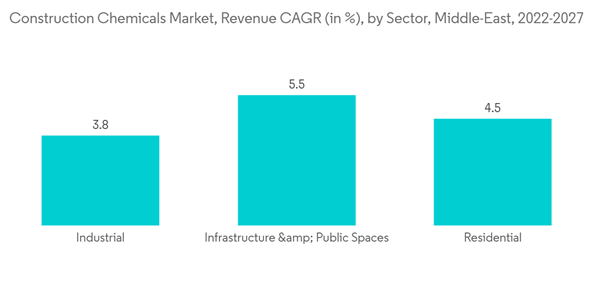

Concrete admixtures held 35.07% of the market share in 2025, with giga-projects pushing performance requirements beyond conventional mixes. Tier-one vendors experiment with nano-silica infusions and CO2-curing accelerators. Waterproofing systems display a 5.32% CAGR through 2031, driven by green-building mandates and increased below-grade structures. Suppliers offer warranties matching 30-year design lives to leverage lifecycle-cost discussions.

Market Landscape

Market Drivers

- Accelerated Infrastructure Spending Under National Vision Programs

- Mandated Adoption of Green Building Rating Systems (e.g., Estidama, GSAS)

- Rise of Giga-Projects Requiring Specialty, High-Performance Admixtures

- Rapid Expansion of Data-Center Construction Needs Antistatic Flooring

- Desalination-Plant Boom Driving Demand for Anti-Corrosion Coatings

Market Restraints

- Tightening VOC-Emission Caps on Solvent-Borne Products

- Supply-Chain Volatility for Key Raw Materials (Epoxy Resins, Polycarboxylates)

- Skilled-Labor Shortages Limiting Correct On-Site Application

Value Chain Analysis

Porter's Five Forces Analysis

Companies Covered:

- Ahlia Chemicals Company

- Akzo Nobel N.V.

- Caparol Paints

- Dow

- GulfBitumen

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Jotun A/S

- LATICRETE International, Inc.

- Mapei S.p.A.

- Pidilite Industries Ltd

- Saint-Gobain

- Saudi Readymix

- Saveto Group

- Sika AG

- The Sherwin-Williams Company

For more information about this report visit https://www.researchandmarkets.com/r/94w3ch

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachments

- Middle East Construction Chemicals Market Construction Chemicals Market Revenue C A G R In By Geography Middle East 2

- Middle East Construction Chemicals Market Construction Chemicals Market Revenue C A G R In By Sector Middle East 2022