Dublin, Nov. 05, 2025 (GLOBE NEWSWIRE) -- The "Australia Programmatic Advertising Market: Trends, Insights, and Growth Opportunities" has been added to ResearchAndMarkets.com's offering.

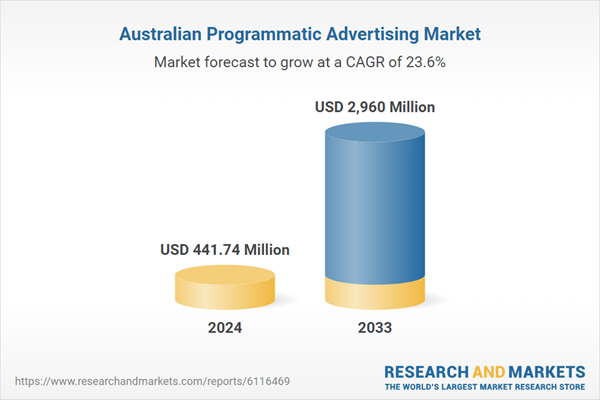

The Australia Programmatic Ad Market is set to rise at US$ 2.96 billion by 2033 from US$ 441.74 million in 2024, with a CAGR of 23.55% from 2025 to 2033. The market is being fueled by increased consumption of digital media, real-time buying of advertisements, and stepped-up spending in data-driven marketing campaigns by brands for highly customized and measurable advertisement results across various platforms.

Growth Drivers for the Australia Programmatic Advertising Market

Increasing Need for Data Marketing

Australian companies are adopting data-driven marketing to improve advertising ROI. Programmatic advertising enables advertisers to use consumer data for real-time targeting by location, browsing activities, and demographics. With customers spending more time on the web, brands feel compelled to personalize advertisements in order to grab attention in an effective manner. This has created a demand for automated, measurable ad platforms, which has increased dramatically. Furthermore, the availability of first-party and third-party data is enabling advertisers to segment audiences precisely, making programmatic a solution of choice for performance-driven campaigns.

In September 2024, TAFE NSW Meadowbank's Institute of Applied Technology Digital (IATD) collaborated with the world's leading analytics provider SAS to counter Australia's increasing data skills shortage. The two have rolled out a 10-week Data Analytics Work Integrated Learning Program with hands-on, industry-relevant skills in data visualization, machine learning, critical thinking, and problem-solving. The program seeks to prepare students with enterprise-ready skills, fostering workforce preparedness in analytics and augmenting NSW's talent pipeline digital capabilities.

Growth in Connected TV and Digital Streaming Platforms

The popularity of Connected TV (CTV) and digital streaming platforms in Australia has created new inventory paths for programmatic advertising. Audiences are increasingly consuming content on platforms such as YouTube, Netflix, and in-market streaming services on smart TVs and smartphones. Programmatic technology allows brands to put dynamic ads within these platforms and typically target viewers based on behavioral signals. As ad budgets move from linear TV to digital platforms, programmatic CTV ad spending is forecast to increase substantially, driving market growth across retail, financial, and entertainment sectors. In March 2025, Warner Bros. Discovery's streaming platform Max will debut direct to consumer in Australia.

Rising Mobile and Social Media Penetration

With one of the world's highest smartphone penetration rates, Australia makes mobile a must-have channel for advertisers. Mobile programmatic allows for location targeting and real-time interaction. Social media sites including Facebook, Instagram, and TikTok provide strong programmatic capabilities through their ad networks. As consumers spend significant time on mobile apps and social media, advertisers are shifting budgets to mobile-first programmatic buying. This movement is fueling creativity in ad formats (native, video) and increasing demand for mobile-led programmatic platforms. In early 2025, Australia had 34.4 million active cellular mobile connections, which was 128 percent of its population. Some connections might have only voice and SMS services, but no internet access.

Difficulties in the Australia Programmatic Advertising Industry

Data Privacy and Regulatory Compliance Concerns

As more attention is being paid to how user data is gathered and utilized in advertising, privacy legislation such as Australia's Privacy Act and compliance with international standards (e.g., GDPR) is affecting the programmatic landscape. Marketers need to ensure their campaigns align with consent and data protection guidelines. The elimination of third-party cookies is also introducing uncertainty. These developments force advertisers to make a transition towards first-party data strategies, but many companies remain unready, thus slowing the adoption rate.

Ad Fraud and Transparency

Ad fraud continues to be an issue in Australia's programmatic advertising economy. Activities such as domain spoofing, click fraud, and spurious impressions lower ROI and erode trust. Also, the multi-step nature of programmatic supply chains engenders opacity, and advertisers find it hard to track specifically where their ads are appearing. This transparency gap results in inefficiencies and mistrust among buyers and sellers. Although technologies like ads.txt and blockchain are being explored, widespread implementation is still evolving, posing a barrier to optimal programmatic utilization.

Key Attributes

| Report Attribute | Details |

| No. of Pages | 200 |

| Forecast Period | 2024-2033 |

| Estimated Market Value (USD) in 2024 | $441.74 Million |

| Forecasted Market Value (USD) by 2033 | $2.96 Billion |

| Compound Annual Growth Rate | 23.5% |

| Regions Covered | Australia |

Key Topics Covered

1. Introduction

2. Research & Methodology

3. Executive Summary

4. Market Dynamics

4.1 Growth Drivers

4.2 Challenges

5. Australia Programmatic Advertising Market

5.1 Historical Market Trends

5.2 Market Forecast

6. Market Share Analysis

6.1 Type

6.2 Auction

6.3 Platform

6.4 Ad Format

6.5 End Use

6.6 By States

7. Type

7.1 Movement-based advertising

7.2 Movement-based publicizing

8. Auction

8.1 Real-Time Bidding (RTB)

8.2 Private Marketplace (PMP)

8.3 Programmatic Direct

8.4 Preferred Deals

9. Platform

9.1 Desktop

9.2 Mobile

9.3 Video

9.4 Social Media

10. Ad Format

10.1 Display

10.2 Video

10.3 Native

10.4 Audio

11. End Use

11.1 Retail & Consumer Goods

11.2 BFSI

11.3 Media & Entertainment

11.4 Telecom & Communication

11.5 Healthcare

11.6 Hospitality

11.7 Education

11.8 Others

12. Top States

12.1 New South Wales

12.2 Victoria

12.3 Queensland

12.4 Western Australia

12.5 South Australia

12.6 Australian Capital Territory

12.7 Tasmania

12.8 Northern Territory

13. Value Chain Analysis

14. Porter's Five Forces Analysis

14.1 Bargaining Power of Buyers

14.2 Bargaining Power of Suppliers

14.3 Degree of Competition

14.4 Threat of New Entrants

14.5 Threat of Substitutes

15. SWOT Analysis

15.1 Strength

15.2 Weakness

15.3 Opportunity

15.4 Threats

16. Pricing Benchmark Analysis

17. Key Players Analysis

17.1 Alphabet Inc. (Google LLC)

17.2 Meta (Facebook)

17.3 Amazon.com, Inc.

17.4 Microsoft

17.5 Alibaba Group Holding Limited

17.6 Adobe

17.7 The Trade Desk

For more information about this report visit https://www.researchandmarkets.com/r/s0ltj6

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment