Dublin, Oct. 29, 2025 (GLOBE NEWSWIRE) -- The "United States Personal Computer Market Report by Form Factor, End User, Processor Architecture, Price Band, Distribution Channel, Operating System, States and Company Analysis, 2025-2033" has been added to ResearchAndMarkets.com's offering.

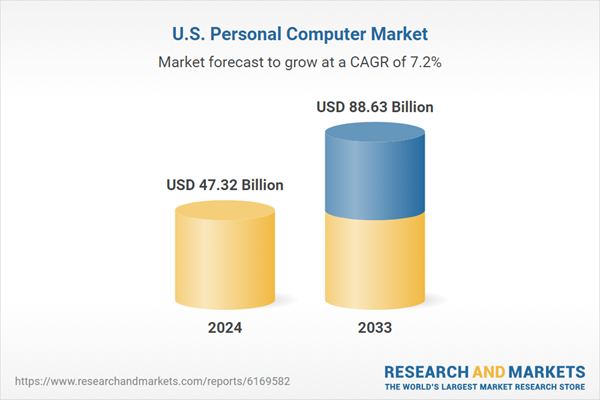

The US Personal Computer Market is estimated to grow substantially from US$ 47.32 billion in 2024 to US$ 88.63 billion during 2033. This expansion signifies a Compound Annual Growth Rate (CAGR) of 7.22% during 2025-2033. The reasons for this growth include improvements in technology, growing demand for work-from-home solutions, and an expanding need for high-performance computing systems across different industries.

The increased popularity of remote work, online learning, and online communication has made PCs necessary tools for productivity. The gaming market has also created a demand for high-performance PCs, reinforcing their importance in American households. As technology evolves, personal computers continue to be integral in people's lives, adapting to the changing needs of users nationwide.

Blended work patterns and virtual learning have irreversibly elevated the status of personal computers in American businesses and homes. Workers require high-performance laptops and desktops tuned for video conferencing, multitasking, and cloud collaboration. Students, from K-12 to university levels, increasingly use budget notebooks or Chromebooks for accessing class materials and digital tools. Despite the reopening of offices, businesses continue investing in refresh cycles to provide distributed teams with uniform devices. Better webcams, extended battery life, and slim designs have become purchasing priorities. This is a sustainable behavioral change that guarantees steady, regular demand, particularly with organizations embracing device-as-a-service (DaaS) models that package PCs, security, and support together. In February 2024, ASUS introduced the newest BR series ruggedized laptops for K-12 Education, designed to withstand daily classroom challenges and exemplify the company's commitment to user-focused design and reliability.

Gaming, streaming, and content creation continue to drive growth in the U.S. PC market. Enthusiasts require high-GPU systems with sophisticated cooling, high-refresh monitors, and customizable builds. Esports, 4K/8K video editing, and VR use cases drive performance requirements beyond mainstream consumer PCs. Simultaneously, platforms like Twitch, YouTube, and TikTok have cultivated a mainstream acceptance of content creation, making advanced PCs productivity tools for younger audiences. Accessory ecosystems-keyboards, monitors, headsets-extend revenue opportunities further. PC vendors benefit from cross-industry innovation, as AI-powered applications in Adobe Creative Cloud and real-time rendering engines become mainstream. The creator and gaming economies keep high-end desktop and laptop segments stable, regardless of overall industry movements. In January 2025, Lenovo unveiled the newest additions to its Lenovo Legion gaming device, accessory, and software ecosystem at CES 2025, offering a wide range of devices in various form factors to provide gamers of all levels with powerful solutions for reaching their potential.

Breakthroughs in chip design are transforming U.S. PC performance and efficiency. ARM-based processors offer phenomenal battery life, instant-on capability, and robust performance per watt, attracting mobile professionals. Concurrently, x86 suppliers are enhancing multicore efficiency and AI acceleration, enabling PCs to handle demanding software processing locally. Ultrabooks, foldables, and 2-in-1 configurations provide portability without sacrificing capability, broadening appeal among professionals and students alike. AI-enhanced features like voice transcription, background noise canceling, and predictive battery optimization improve user experiences. Hardware-software integration-particularly within ecosystem lock-ins among devices, OS, and cloud platforms-encourages more frequent upgrades by consumers.

Despite recovery efforts, the U.S. PC industry continues to experience bottlenecks in semiconductor supplies, logistics, and component pricing. Graphics cards, memory modules, and high-end processors are often in short supply, leading to price instability. Tariffs, geopolitical risks, and cargo delays exacerbate procurement challenges for distributors and OEMs. These issues compress margins and complicate inventory planning, particularly for smaller companies less able to withstand volatility compared to larger vendors. As manufacturers diversify supply bases, the prospect of continued disruptions remains a pressing challenge.

Smartphones and tablets continue to compete with low-end PCs for light use cases, such as web browsing, streaming, and social networking. Tablets equipped with high-end features, keyboard detachability, and stylus support challenge notebooks in educational contexts and general light productivity. Mobile-first applications and cloud services reduce the necessity for full PCs for much of the user base. This competition forces PC makers to vie on performance, ecosystem integration, and security. For consumers prioritizing portability and price, mobile devices often suffice, decelerating PC replacement cycles and constraining growth within the budget segment.

Key Attributes

| Report Attribute | Details |

| No. of Pages | 200 |

| Forecast Period | 2024-2033 |

| Estimated Market Value (USD) in 2024 | $47.32 Billion |

| Forecasted Market Value (USD) by 2033 | $88.63 Billion |

| Compound Annual Growth Rate | 7.2% |

| Regions Covered | United States |

Key Topics Covered

1. Introduction

2. Research & Methodology

3. Executive Summary

4. Market Dynamics

4.1 Growth Drivers

4.2 Challenges

5. United States Personal Computer Market

5.1 Historical Market Trends

5.2 Market Forecast

6. Market Share Analysis

6.1 By Form Factor

6.2 By End User

6.3 By Processor Architecture

6.4 By Price Band

6.5 By Distribution Channel

6.6 By Operating System

6.7 By States

7. Form Factor

7.1 Laptops / Notebooks

7.2 Desktop Towers and SFF

7.3 All-in-One PCs

7.4 Tablets / Detachables

8. End User

8.1 Consumer

8.2 Small and Medium Business

8.3 Large Enterprise

8.4 Government and Education

9. Processor Architecture

9.1 x86 (Intel-AMD)

9.2 ARM-based

9.3 RISC-V & Others

10. Price Band

10.1 Entry-Level (< USD 600)

10.2 Mid-Range (USD 600-1200)

10.3 Premium / Gaming (> USD 1200)

11. Distribution Channel

11.1 Offline Retail and VARs

11.2 E-commerce and Direct-to-Consumer

12. Operating System

12.1 Windows

12.2 macOS

12.3 ChromeOS

12.4 Linux Distros

13. Top States

13.1 California

13.2 Texas

13.3 New York

13.4 Florida

13.5 Illinois

13.6 Pennsylvania

13.7 Ohio

13.8 Georgia

13.9 New Jersey

13.10 Washington

13.11 North Carolina

13.12 Massachusetts

13.13 Virginia

13.14 Michigan

13.15 Maryland

13.16 Colorado

13.17 Tennessee

13.18 Indiana

13.19 Arizona

13.20 Minnesota

13.21 Wisconsin

13.22 Missouri

13.23 Connecticut

13.24 South Carolina

13.25 Oregon

13.26 Louisiana

13.27 Alabama

13.28 Kentucky

13.29 Rest of United States

14. Value Chain Analysis

15. Porter's Five Forces Analysis

15.1 Bargaining Power of Buyers

15.2 Bargaining Power of Suppliers

15.3 Degree of Competition

15.4 Threat of New Entrants

15.5 Threat of Substitutes

16. SWOT Analysis

16.1 Strength

16.2 Weakness

16.3 Opportunity

16.4 Threats

17. Pricing Benchmark Analysis

17.1 Lenovo Group Limited

17.2 HP Inc.

17.3 Dell Technologies Inc.

17.4 Apple Inc.

17.5 Acer Incorporated

17.6 Microsoft Corporation

17.7 Samsung Electronics Co., Ltd.

17.8 Huawei Technologies Co., Ltd.

17.9 Xiaomi Corporation

17.10 LG Electronics Inc.

18. Key Players Analysis

18.1 Lenovo Group Limited

18.2 HP Inc.

18.3 Dell Technologies Inc.

18.4 Apple Inc.

18.5 Acer Incorporated

18.6 Microsoft Corporation

18.7 Samsung Electronics Co., Ltd.

18.8 Huawei Technologies Co., Ltd.

18.9 Xiaomi Corporation

18.10 LG Electronics Inc.

For more information about this report visit https://www.researchandmarkets.com/r/mfuo1l

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment